The $18.8 Trillion Problem

A Splitting Economy

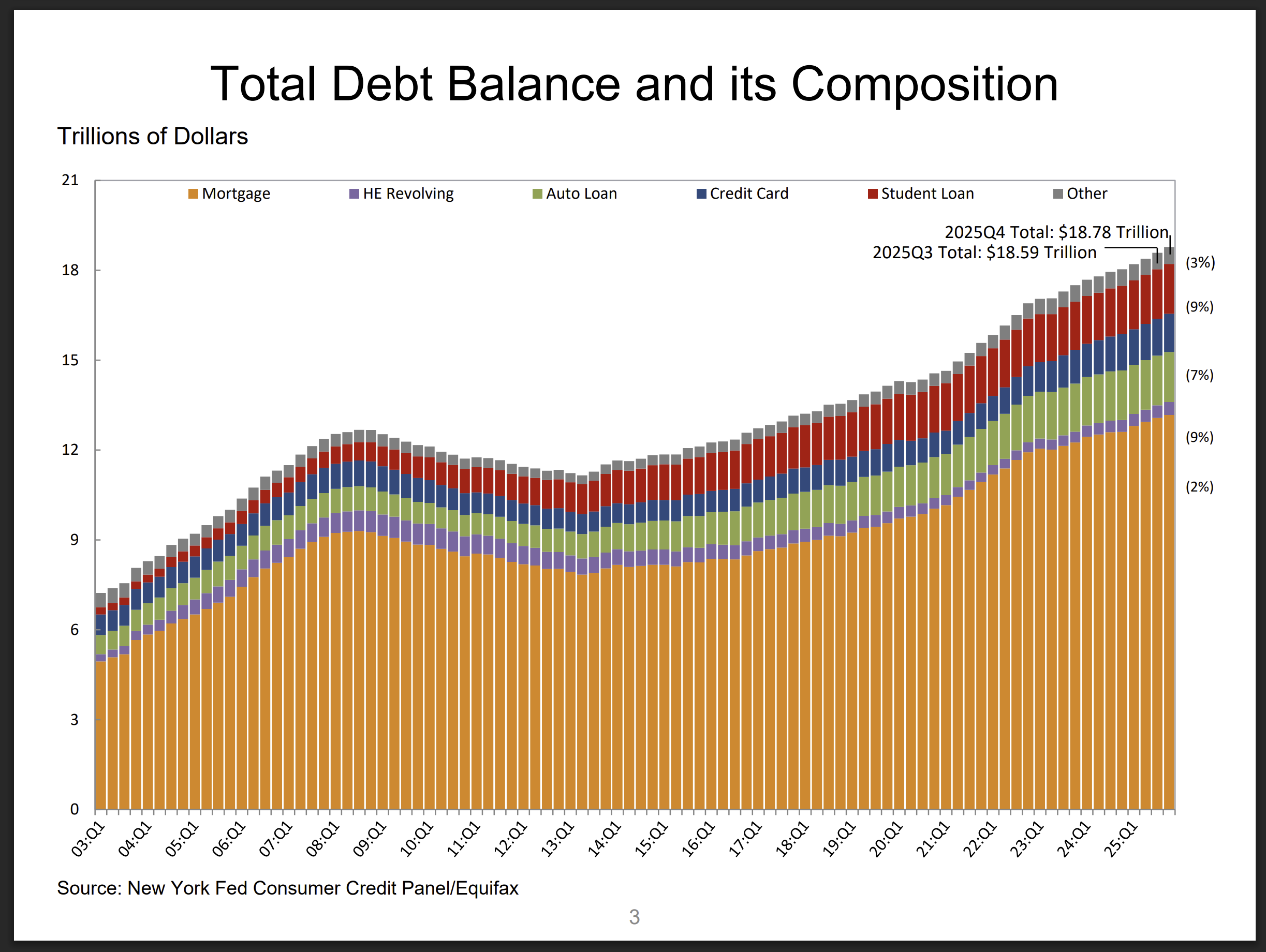

In the fourth quarter of 2025, total U.S. household debt crossed a staggering new threshold: $18.8 trillion.

Read the headline numbers in isolation, and it is easy to find optimists spinning this as a victory. A mountain of debt, some economists argue, is simply the byproduct of a confident consumer base, robust spending, and a healthy economy. But if you look beneath the surface of the aggregate data, a much darker reality takes shape. This is not a story of widespread prosperity driving discretionary borrowing; it is a story of survival.

What the latest figures actually reveal is the stark entrenchment of a “K-shaped” consumer economy. We are looking at two entirely different financial realities diverging in real time.

On the upward arm of the “K,” wealthy households are actively insulated, strategically leveraging their assets and home equity to maintain their lifestyles and build wealth at relatively manageable costs. On the downward arm, the middle and lower-middle classes are absorbing the cumulative, compounding weight of multi-year inflation. Exhausting their pandemic-era buffers, they are now reliant on punishingly expensive, high-interest credit cards just to tread water and cover everyday essentials.

The Federal Reserve Bank of New York’s Q4 2025 Household Debt and Credit Report data is concerning through this lens.

We are no longer looking at one unified American consumer, but two distinct classes moving rapidly in opposite financial directions, with the “winning” class getting ever smaller at an accelerating rate.

The Top of the “K”: Wealth, Equity, and the Homeowner’s Buffer

To understand the upward arm of the “K-shaped” economy, you have to look at the homeowners. For this demographic—which skews older and higher-income—the current economic environment is less of a crisis and more of a strategic maneuvering exercise.

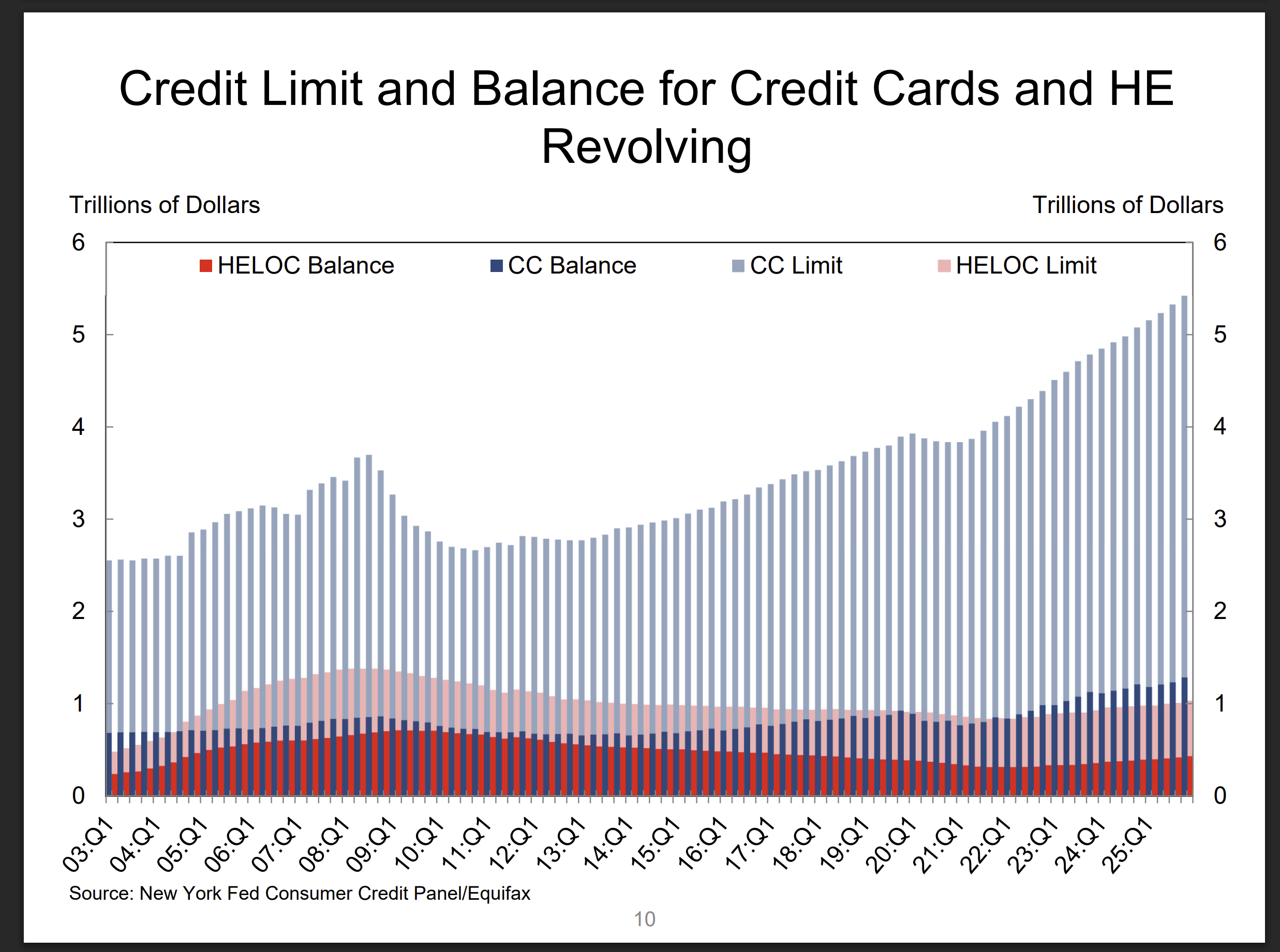

The Q4 2025 data paints a picture of a well-insulated class utilizing their assets to their advantage. Home Equity Line of Credit (HELOC) balances rose for the 15th consecutive quarter, reaching $433 billion. At the same time, banks expanded HELOC limits by an additional $25 billion.

Why is this significant? Because the vast majority of these homeowners locked in historically low, fixed-rate mortgages years ago, effectively shielding their largest monthly expense from recent interest rate hikes. Meanwhile, the value of their homes has surged. They are now sitting on massive equity reserves.

When these consumers face inflationary pressures or want to fund large expenses like home renovations, they aren’t forced into the punishing 20-plus percent APRs of the credit card market. Instead, they tap into their home equity. This secured borrowing acts as a crucial financial buffer, allowing them to manage cash flow, consolidate other debts, and maintain their standard of living at a fraction of the borrowing cost.

As the chart above illustrates, while both HELOC and credit card limits are expanding, the nature of that borrowing is fundamentally different. The steady, secured borrowing of the wealthy stands in stark contrast to the volatile spike in unsecured credit card reliance happening just down the economic ladder.

The Bottom of the “K”: The Middle-Class Credit Card Trap

If the top of the “K” is defined by strategic asset leveraging, the bottom is defined by a growing reliance on unsecured debt just to survive.

The Q4 2025 data reveals a breaking point for the middle and lower-middle classes. Credit card balances have surged to a record-breaking $1.28 trillion, marking a 5.5% increase year-over-year. Crucially, it is not just the total balance that is growing; there is a steady, undeniable climb in the sheer number of active credit card accounts across the country.

It is vital to understand why this explosion in unsecured debt is happening. The narrative that this represents a confident consumer on a post-pandemic spending spree on luxury goods or vacations is fundamentally flawed. Instead, this is the mathematical consequence of cumulative inflation steadily outpacing wage growth for average earners.

As the excess savings accumulated during the pandemic were finally exhausted, middle-class households hit a wall. To bridge the widening gap between their stagnant paychecks and the inflated costs of rent, groceries, insurance, and utilities, these consumers have become structurally reliant on credit cards. They are no longer using plastic for discretionary upgrades; they are using it to cover everyday life.

As the chart above starkly illustrates, the steep and sustained climb in credit card accounts tells the story of a demographic increasingly turning to high-interest debt to make ends meet. For these households, the credit card is no longer a convenience—it is a lifeline.

The Tipping Point: Runaway Compounding and Rising Delinquencies

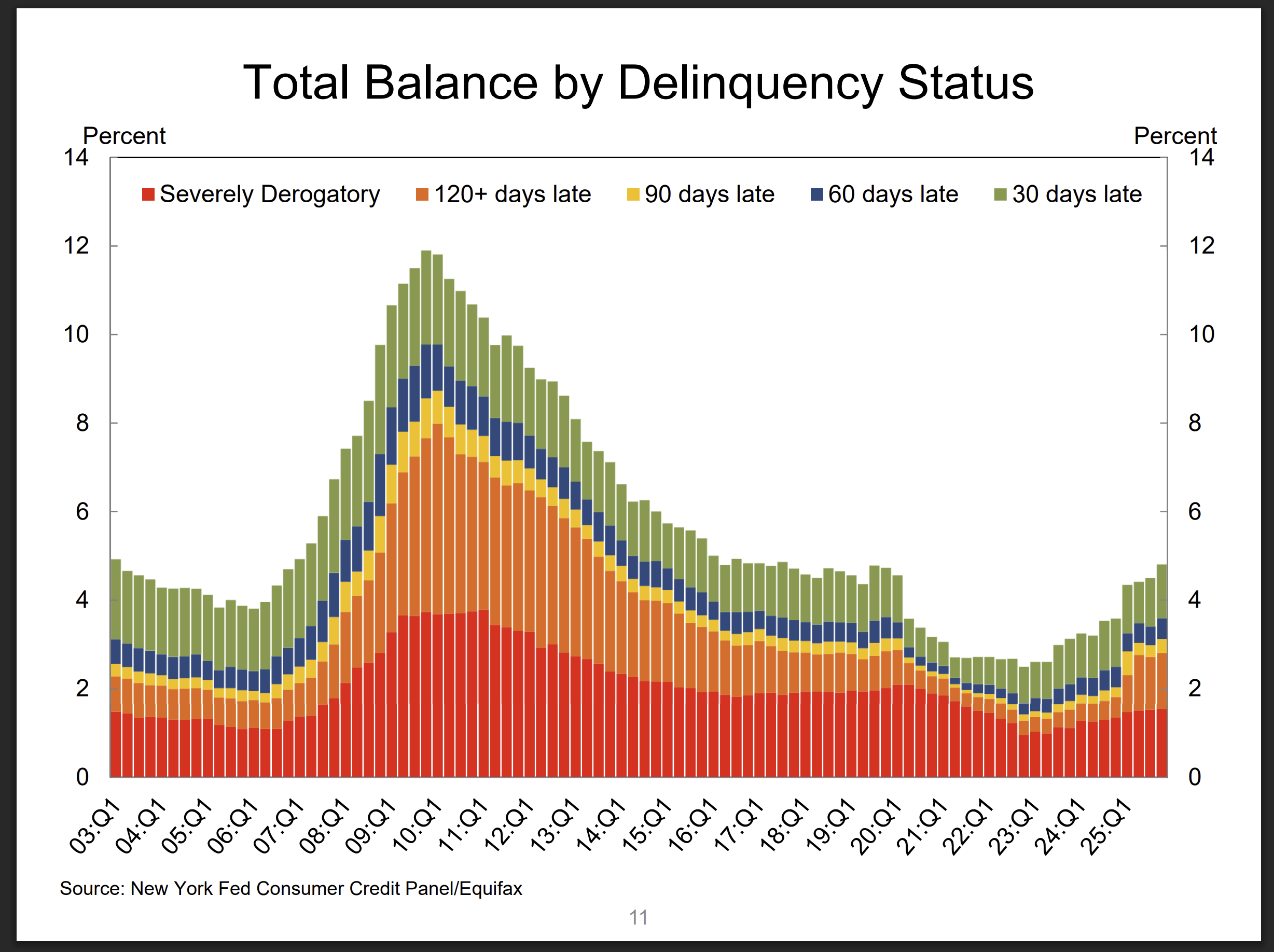

The most alarming takeaway from the Q4 2025 data isn’t just the sheer volume of debt—it’s the undeniable evidence that millions of consumers are failing to keep up with it. We have reached the tipping point where borrowing to survive transitions into a runaway compounding crisis.

The core warning sign flashes in the aggregate delinquency rate, which worsened to 4.8% by the end of the year. But the true severity of the situation is found in the specific pain points hidden within that average. Lenders are subtly loosening credit standards just to maintain volume, with the median credit score for new auto loans dropping and the bottom-tier threshold for mortgages sliding downward.

However, the most devastating blow came from the student loan sector. Delinquency rates for student loans remain elevated at a massive 9.6%, with approximately one million borrowers falling more than 120 days past due and having their loans transferred to the Default Resolution Group.

For many stretched households, the resumption of student loan payments acted as the final straw. Forced to juggle these reinstated bills alongside inflated costs for rent and food, budgets simply snapped. Consumers leaned heavily on their credit cards to bridge the gap, but the math of minimum payments on high-APR cards is unforgiving. When a borrower is only making the minimum payment on a growing balance with an interest rate north of 20%, the debt aggressively compounds. Once a consumer hits the 90- or 120-day late mark, escaping the debt spiral becomes mathematically improbable.

Take a close look at the chart above. The growing yellow (90 days late) and orange (120+ days late) bars are the visual representation of this compounding trap. It is vital to understand that these late stages of delinquency do not represent forgotten bills or minor budgeting errors. They represent structural defaults—households that have hit a definitive financial wall and simply do not have the capital to service their debt.

Macro Spillover: Why the Broader Economy Should Care

It is easy for those insulated at the top of the economic ladder to view rising credit card delinquencies as a localized problem—a misfortune for the lower-middle class that doesn’t impact the broader financial system. But the “K-shaped” economy does not just apply to consumers; it is rapidly reshaping the corporate landscape as well.

The ripple effect of this localized debt crisis is already washing over corporate profits. While high-end luxury brands, premium travel operators, and top-tier tech companies continue to post strong earnings—buoyed by the wealthy households actively leveraging their assets—businesses that rely on the middle class are facing a brutal environment.

We are seeing a clear divergence in the market. Mass-market retailers, fast-casual dining chains, and subprime auto lenders are staring down shrinking foot traffic, squeezed margins, and rising default rates. When a household is forced to prioritize a 25% APR credit card minimum payment just to keep their accounts in good standing, the first things slashed from the budget are restaurant dinners, new clothes, and discretionary retail purchases.

This brings us to the ultimate macroeconomic warning. Consumer spending historically accounts for roughly 70% of the U.S. economy. You cannot have the bottom 60% of earners systematically directing larger and larger portions of their monthly income purely toward debt servicing without a profound cost to the broader market. As discretionary spending among the middle class inevitably craters under the weight of this $1.28 trillion credit card mountain, it threatens to act as an anchor, dragging down broader economic growth and corporate earnings right along with it.

Conclusion: A Fractured Foundation and the AI Illusion

This widening fracture demands urgent policy intervention before the cracks become irreparable. Policymakers could start by addressing the root causes: reinstating targeted relief for student loans, such as broader forgiveness programs or income-driven repayment caps tied to inflation. On the credit front, capping credit card APRs at 15%—as some progressive proposals suggest—would ease the compounding trap for middle-class borrowers. Meanwhile, bolstering wage growth through minimum wage hikes or tax credits for low earners could close the inflation-wage gap. Without such measures, the Fed’s interest rate tinkering alone risks exacerbating the divide, as cuts might fuel asset bubbles at the top while leaving the bottom mired in high-cost debt.

Ultimately, the Q4 2025 household debt report destroys the myth of the “average” American consumer. There is no monolith. Instead, we have a deeply fractured foundation where $18.8 trillion in debt is distributed across two entirely different financial realities.

For the moment, the headline economic numbers remain seemingly resilient, propped up almost entirely by the top arm of the “K.” But a closer look at that upper tier reveals its own precarious vulnerabilities. The broader economy is increasingly hanging by a thread woven by the “Magnificent 7” tech giants and a historic wave of AI speculation. We are witnessing a massive, circular loop of funding and valuation: tech companies pouring billions into AI infrastructure, government subsidies fueling domestic tech manufacturing, and institutional investors driving up the stock market to unprecedented heights.

This raises a terrifying question: What if the top of the “K” is just as over-leveraged as the bottom, only on future productivity rather than credit cards?

Even if we assume the AI boom is not a bubble—if the massive bets pay off and the technology reshapes global commerce—we must ask where the bottom of the “K” fits into that future. Proponents argue that a rising tide of technological innovation lifts all boats. Yet, the wealth hasn’t trickled down so far; it has only concentrated further. More alarmingly, if AI successfully delivers the corporate efficiencies it promises, it will do so by automating the very jobs that the middle and lower-middle classes rely on to service their compounding debt.

Consider the concrete bets fueling this loop: In 2025 alone, companies like Nvidia and OpenAI funneled over $100 billion into AI chips and data centers, subsidized by CHIPS Act billions, while stock valuations soared on promises of 10x productivity gains. Yet, early indicators from sectors like customer service and logistics show AI displacing roles—McKinsey estimates up to 45% of U.S. jobs could be automated by 2030, hitting administrative and retail workers hardest. For debt-burdened households, this isn’t innovation; it’s a double bind, where surviving today means borrowing against a tomorrow with fewer paychecks.

We are faced with a stark dual-failure path. If the AI bubble bursts, the top of the “K” collapses, wiping out the asset wealth that has been artificially inflating the broader economy. If the AI bet succeeds, it risks displacing millions of workers, accelerating the insolvency of the bottom of the “K.”

In many ways, the structural rot carries distinct echoes of 2008. Back then, the crisis began with subprime mortgages at the bottom of the economic ladder, a vulnerability that was ignored until it triggered a catastrophic collapse of the over-leveraged institutions at the top. Today, the subprime rot is in auto loans, student debt, and a record $1.28 trillion in credit card balances.

The U.S. economy is currently attempting a dangerous balancing act. But mathematics is unforgiving. No matter how much wealth is generated at the absolute top, the upper arm of the “K” cannot indefinitely drag an increasingly insolvent, debt-burdened bottom half forward. Eventually, the foundation cracks.

Looking ahead to 2026, early indicators suggest the divide may deepen: Preliminary Q1 data hints at continued credit card spikes amid cooling job growth, while AI-driven markets teeter on overvaluation. Investors and consumers may need to brace for volatility—diversifying away from tech-heavy portfolios at the top, and building emergency funds or seeking debt consolidation at the bottom. The question isn’t if the K bends further, but how far before it breaks.

You are right that this is very redolent of the early 2008 period wherein rising mortgage defaults were ignored at best and derided as irrelevant by many. Rising credit card defaults will crash that market just as surely if the current trends are not reversed, and soon.

As always, who is receiving the benefits, and who will pay the price, are the pertinent questions.